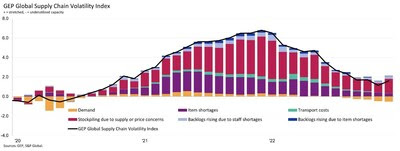

The GEP Global Supply Chain Volatility Index — a leading indicator tracking demand conditions, shortages, transportation costs, inventories and backlogs — shows declining demand for raw materials, commodities, and other components needed to provide finished goods and services in December, reflecting the growing risk of a recessionary period ahead.

Additionally, more businesses are safety stockpiling inventories, particularly in Europe and North America, due to a resurgence in COVID-19 infections in China and increased concerns about future supply and pricing, partly reversing destocking efforts seen in the prior six months.

As a result of greater safety stockpiling and worsening of labor shortages, the GEP Global Supply Chain Volatility Index rose — up from 1.15 in November to 1.61 in December — halting the improvements in the world’s supply chains, which began in the summer of 2022.

Commenting on the latest results, John Piatek, GEP’s vice president of consulting, said: “We are shifting from a sellers’ to a buyers’ market, and companies should be pushing back hard on all price increases from their suppliers, which will continue to drive down inflation. Falling demand signals the increasing likelihood of a global recession in the first half of 2023.”

The key findings from December’s report:

- DEMAND: Demand for components, raw materials, commodities and any other items companies need to provide their goods and services declined further in December, especially in North America.

INVENTORIES: Global business reports of safety stockpiling are up since November, which is a key factor behind December’s increase in GEP’s Global Supply Chain Volatility Index.

LABOR SHORTAGES: Companies report an uptick in labor shortages, causing supplier capacity to be stretched.

MATERIAL SHORTAGES: Global supply shortages are at their lowest level since September 2020 as suppliers continue to adjust to market conditions. Easing demand has reduced competition for items.

TRANSPORTATION: Transportation costs are at their lowest in over two years, highlighting weaker pressures on shipping, train, air and road freight.

REGIONAL SUPPLY CHAIN VOLATILITY: Supply chains feeding into Europe remain the most stretched, compared to Asia and North America, in December.

ABOUT THE GEP GLOBAL SUPPLY CHAIN VOLATILITY INDEX

The GEP Global Supply Chain Volatility Index is produced by S&P Global and GEP. The GEP Global Supply Chain Volatility Index is derived from S&P Global’s PMI™ surveys, sent to companies in over 40 countries, totaling around 27,000 companies. These countries account for 89% of global gross domestic product (GDP) (source: World Bank World Development Indicators).

The headline figure is the GEP Global Supply Chain Volatility Index. This a weighted sum of six sub-indices derived from PMI data, PMI Comments Trackers and PMI Commodity Price & Supply Indicators compiled by S&P Global.

The GEP Global Supply Chain Volatility Index is calculated using a weighted sum of the z-scores of the six indices. Weights are determined by analyzing the impact each component has on suppliers’ delivery times through regression analysis.

The six variables used are 1) JP Morgan Global Quantity of Purchases Index, 2) All Items Supply Shortages Indicator, 3) Transport Price Pressure Indicator, and Manufacturing PMI Comments Tracker data for 4) stockpiling due to supply or price concerns, and backlogs rising due to 5) staff shortages and 6) item shortages.

A value above 0 indicates that supply chain capacity is being stretched and supply chain volatility is increasing. The further above 0, the greater the extent to which capacity is being stretched.

A value below 0 indicates that supply chain capacity is being underutilized, reducing supply chain volatility. The further below 0, the greater the extent to which capacity is being underutilized.

A Supply Chain Volatility Index is also published at a regional level for Europe, Asia, North America and the UK. The regional indices measure the performance of supply chains connected to those parts of the world.